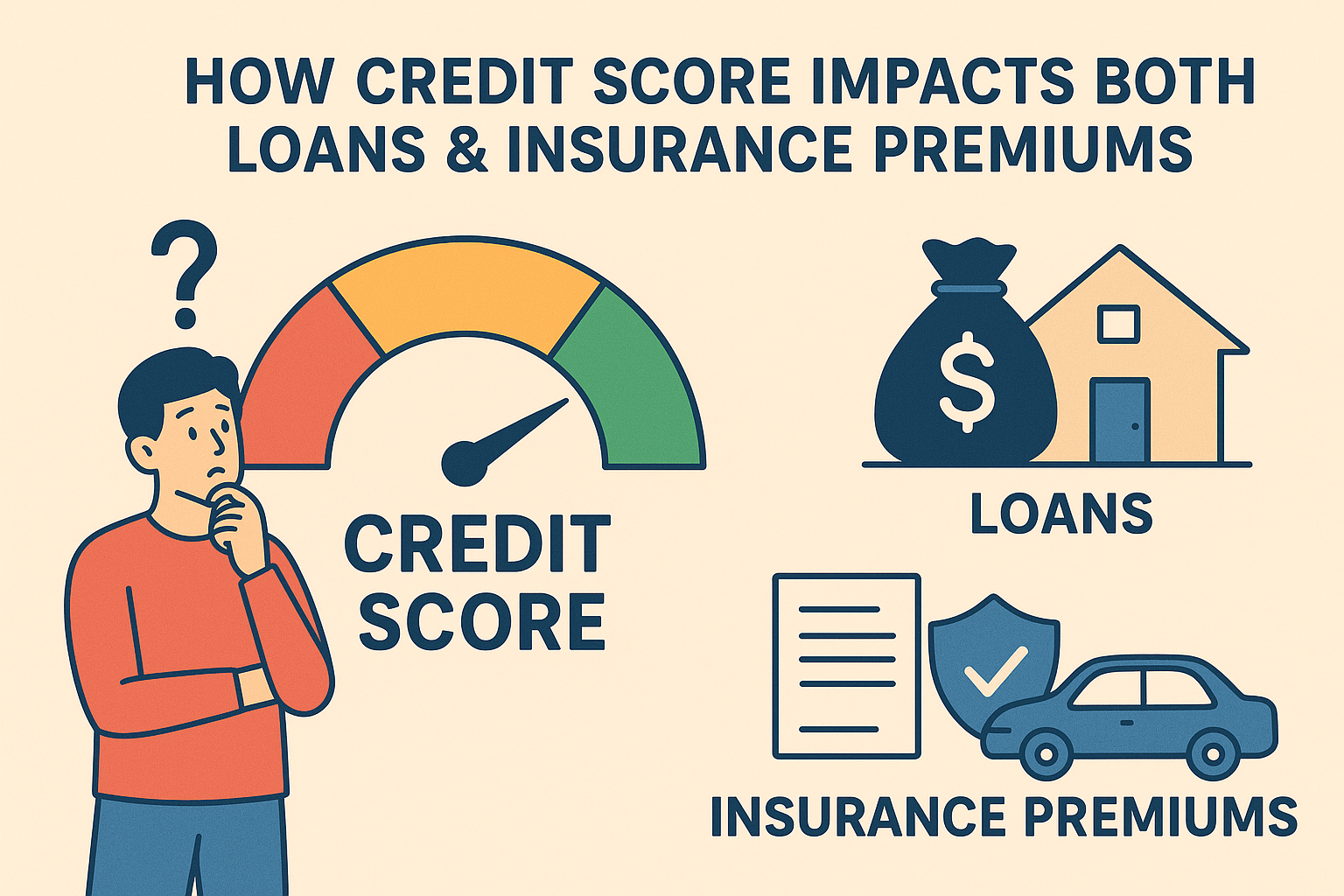

What is a Credit Score?

A credit score is a three-digit number, typically ranging from 300 to 850, that reflects your creditworthiness. It’s calculated based on your credit history, including payment history, credit utilization, length of credit history, and types of credit used.

- Excellent: 750+

- Good: 700–749

- Fair: 650–699

- Poor: Below 650

The higher your score, the more trustworthy you appear to lenders and insurers.

How Credit Score Affects Loans

When applying for loans—whether a mortgage, auto loan, or personal loan—lenders rely on your credit score to determine:

- Loan Approval – A high score increases your chances of approval, while a low score can lead to rejections.

- Interest Rates – Borrowers with excellent credit often get the lowest interest rates, saving thousands of dollars over the life of the loan.

- Loan Amount – Lenders are more willing to offer larger loan amounts if your credit history is strong.

- Loan Terms – Higher credit scores may result in longer repayment periods with flexible conditions.

Example: Two people apply for a $20,000 car loan. With excellent credit, one gets a 5% interest rate. With poor credit, the other faces 12%. The difference in monthly payments and total interest over time is huge.

How Credit Score Affects Insurance Premiums

Insurance companies, especially in the USA, use a credit-based insurance score to predict the likelihood of filing claims. While not every state allows this practice, many do. Here’s how it impacts premiums:

- Auto Insurance – Drivers with poor credit can pay significantly higher premiums compared to those with excellent credit.

- Home Insurance – A strong credit score can lower homeowner’s insurance costs because insurers see you as less risky.

- Life Insurance – While medical history and age matter most, credit scores can sometimes influence the premium you’re offered.

Example: A driver with poor credit may pay up to 50% more for the same auto insurance coverage compared to someone with excellent credit.

Why Insurers and Lenders Care About Credit Scores

- For Loans: It predicts whether you’re likely to repay on time.

- For Insurance: It suggests how responsible and low-risk you are, which affects the chance of filing claims.

In short, a good credit score saves money on both borrowing and protection.

How to Improve Your Credit Score

If your score isn’t where you want it, here are proven steps to boost it:

- Pay bills on time – Payment history is the biggest factor.

- Keep credit utilization low – Try to use less than 30% of your available credit.

- Avoid too many new accounts – Multiple hard inquiries can lower your score.

- Monitor your credit report – Check for errors and dispute them.

- Build a long credit history – Keep older accounts open.

Improving your score not only secures better loans but also reduces insurance costs.

Final Thoughts

Your credit score impacts both loans and insurance premiums in powerful ways. Maintaining a strong score means more loan approvals, lower interest rates, and affordable insurance coverage. Every American can benefit from understanding and improving their credit health.

FAQs

1. What credit score do you need for the best loan rates?

Generally, a score above 740 qualifies you for the best interest rates.

2. Do all states use credit scores for insurance premiums?

Not all. States like California, Hawaii, and Massachusetts restrict insurers from using credit scores to set auto insurance rates.

3. Can improving my credit score lower my insurance costs?

Yes. Over time, as your score improves, you may qualify for better insurance premiums.

4. How often should I check my credit score?

At least once a year, though many free services let you check monthly without hurting your score.