When you apply for a loan—whether it’s a mortgage, car loan, personal loan, or even a credit card—your credit score plays a big role in the lender’s decision. Many people know that having a “good” score is important, but they don’t always understand how much of a difference it can make in approval chances, interest rates, and repayment terms.

In this guide, we’ll break down how credit scores affect loans and why managing your credit is so important.

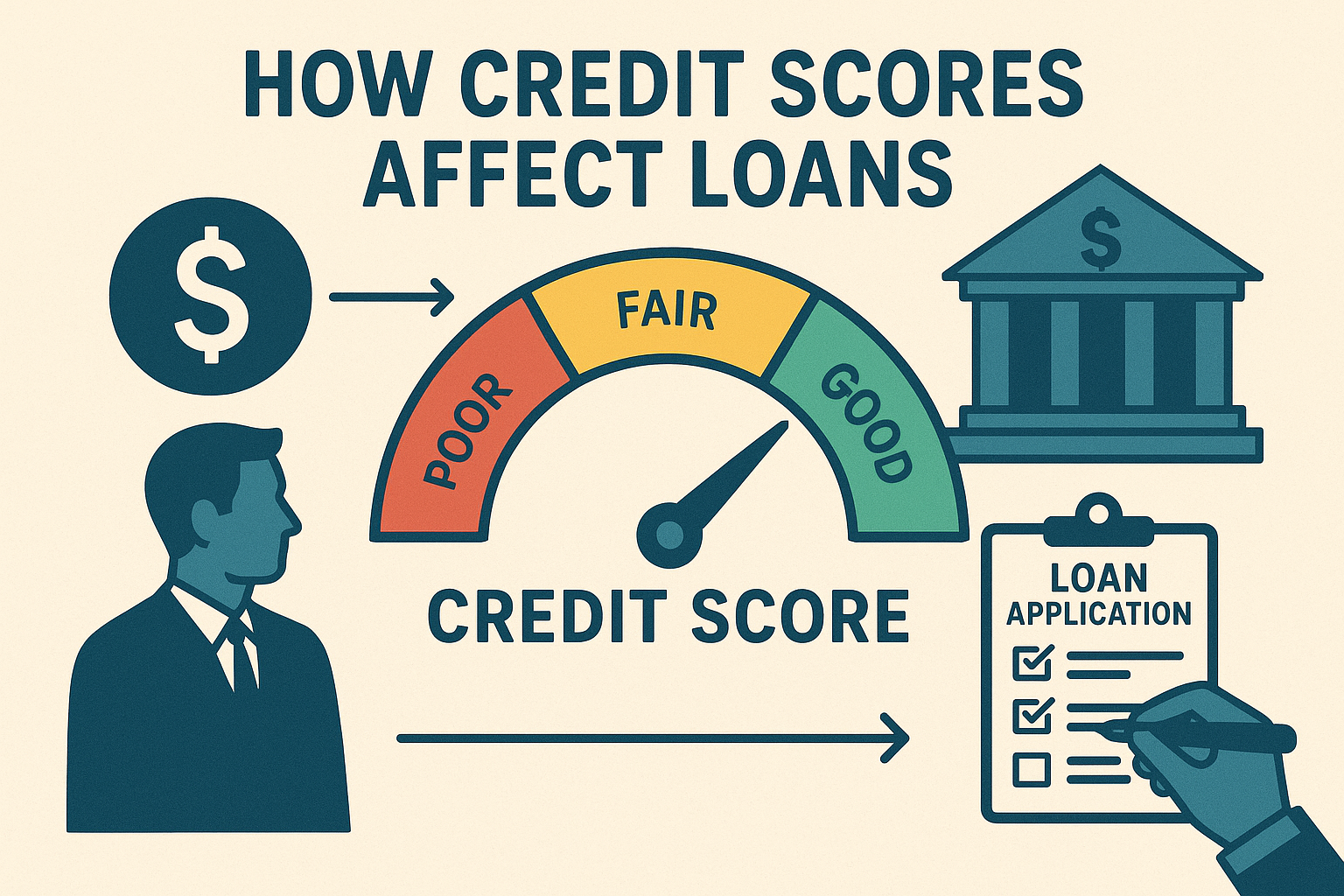

What Is a Credit Score?

A credit score is a three-digit number (usually between 300 and 850 in the U.S.) that reflects your creditworthiness. It’s calculated based on factors such as:

- Payment history – Do you pay bills on time?

- Credit utilization – How much of your available credit are you using?

- Length of credit history – How long you’ve had credit accounts.

- Types of credit – A mix of credit cards, loans, and mortgages.

- Recent inquiries – How often you apply for new credit.

The higher your score, the less risky you appear to lenders.

How Credit Scores Affect Loan Approval

When you apply for a loan, lenders first look at your credit score. Here’s how it impacts approval:

- Excellent Credit (720–850): Very high chance of approval. Lenders see you as low-risk.

- Good Credit (670–719): Strong chance of approval, though terms may be slightly less favorable.

- Fair Credit (580–669): You may still qualify, but lenders could limit your options or require higher interest rates.

- Poor Credit (300–579): High chance of rejection. If approved, loans often come with high rates and strict terms.

How Credit Scores Affect Loan Interest Rates

Interest rates are where your credit score really makes a difference. Even a small change in score can save—or cost—you thousands of dollars over time.

- High credit score: Lenders offer lower interest rates because they trust you’ll repay.

- Low credit score: Lenders charge higher interest rates to cover the risk of default.

Example:

- A borrower with a 750 credit score might get a car loan at 5% interest.

- Another borrower with a 600 credit score might be offered the same loan at 12% interest.

Over the life of the loan, the difference could mean paying thousands more.

How Credit Scores Affect Loan Terms

Besides approval and interest rates, your score also influences loan terms such as:

- Loan amount – Higher scores often qualify for larger loans.

- Repayment period – Good scores may allow longer repayment timelines with better rates.

- Collateral requirements – With poor credit, lenders may ask for extra security or co-signers.

Can You Get a Loan With Bad Credit?

Yes—but it’s harder. If your credit score is low, lenders may:

- Approve only smaller loan amounts.

- Require a higher down payment.

- Charge high fees and interest.

- Ask for a co-signer with better credit.

If you’re in this situation, consider improving your credit score before applying, unless the loan is urgent.

Tips to Improve Your Credit Score Before Applying for a Loan

- Pay bills on time – Even one late payment can hurt.

- Reduce debt – Keep credit card balances below 30% of your limit.

- Don’t apply for too many new accounts at once.

- Check your credit report for errors and dispute inaccuracies.

- Build credit history by keeping older accounts open.

Final Thoughts

Your credit score is more than just a number—it’s the key to unlocking affordable loans and favorable terms. A strong score can save you thousands of dollars, while a weak one can limit your financial options.

If you’re planning to apply for a loan soon, take time to review your credit score and work on improving it. The effort today can mean major savings tomorrow.